Reflections on the ‘Endowment Model’ for Families

Andrew White, Capricorn Private Investments

We have noted increasing commentary of late around the continuing relevance of the Endowment Model, with its reliance on significant allocations to alternative, and often illiquid, investments to generate returns over the long term. The model, as famously developed by David Swensen while managing the Yale Endowment, emphasises the importance of diversification across asset classes and exploiting the illiquidity premium of alternative assets to generate growth through multiple economic cycles, regardless of prevailing market conditions.

Many large family offices and private investment offices may refer to following some version of an ‘endowment-style’ investment approach; there are certainly echoes of this approach in our work with client families, so it is a topic of some relevance for us. At Capricorn Private Investments, we take the model to mean applying a disciplined, long-term approach for our clients by embracing a range of complementary strategies across both traditional and alternative assets. We seek to deliver superior risk-adjusted returns for these clients, typically entrepreneurs and families of substantial wealth by allocating in a concentrated manner to a select group of active managers in whom we have high conviction, remaining mindful of controlling costs.

In short, our view remains that the tenets of the approach are sound, particularly when dealing with institutional pools of capital, but perhaps of less direct relevance when applied to families, whose time horizons and tolerance for illiquidity and complexity are subject to different constraints.

As recently noted in the FT, Swensen’s approach has been “much-emulated, rarely replicated”. The crux of the recent discussion appears to have been whether the espousal of high allocations to private equity remains relevant given far greater ease of access, and indeed outperformance, of cheaper and more liquid public assets. The powerful trends that have been driving disproportionate concentration into US assets and, by extension, the ‘Mag 7’ group of tech stocks, have drawn this dynamic into clear relief. We note, on the back of this year’s volatility, how quickly these trends can reverse; if anything, recent market moves illustrate how a blend of both liquid and illiquid assets can be beneficial for portfolios.

The illiquidity question

Ongoing questioning and testing of theories is a natural part of the evolution of investing, which is both necessary and welcome. Currently, it is the performance of private equity (PE) as a broad asset class – a key pillar for the ‘endowment model’ – which has rightly been subject to such enquiries. The high fee load of typical PE creates a drag effect, which has been compounded by the marked decline in distributions (‘DPI’). This has been primarily due to a collapse in M&A and capital market activity compared with previous years, resulting in longer hold periods for individual portfolio companies, and subsequently lower realisation of returns for investors.

The most pertinent question for us is whether illiquidity premia still exist in today’s higher rate environment to the extent that allocating to such long-term strategies remains justified. Certainly, in some areas of venture capital and private equity, after fees and lock-ups are taken into account, the answer is no.

At present, we are more inclined to increase our ‘alternative’ allocations to private credit and absolute return strategies, which have consistently delivered 8-9% net returns with (typically) monthly or quarterly liquidity.

We expect to continue to allocate to private equity and other illiquid strategies on a selective basis where appropriate for our mandates, and where we feel the fees are justified by the potential for outsized returns. This is clearly difficult to judge ex ante. For example, we see secondaries, US lower middle market buyouts, and select co-investments (which tend to attract no additional management fees), as attractive strategies still. We have renewed our focus on our expected returns for PE relative to other high-returning asset classes, with a preference for funds with shorter investment periods where possible. The true value of the illiquidity premium remains one of the primary considerations when assessing specific funds for our portfolios, and fundamentally underscores the value of manager and fund selection in illiquid asset classes.

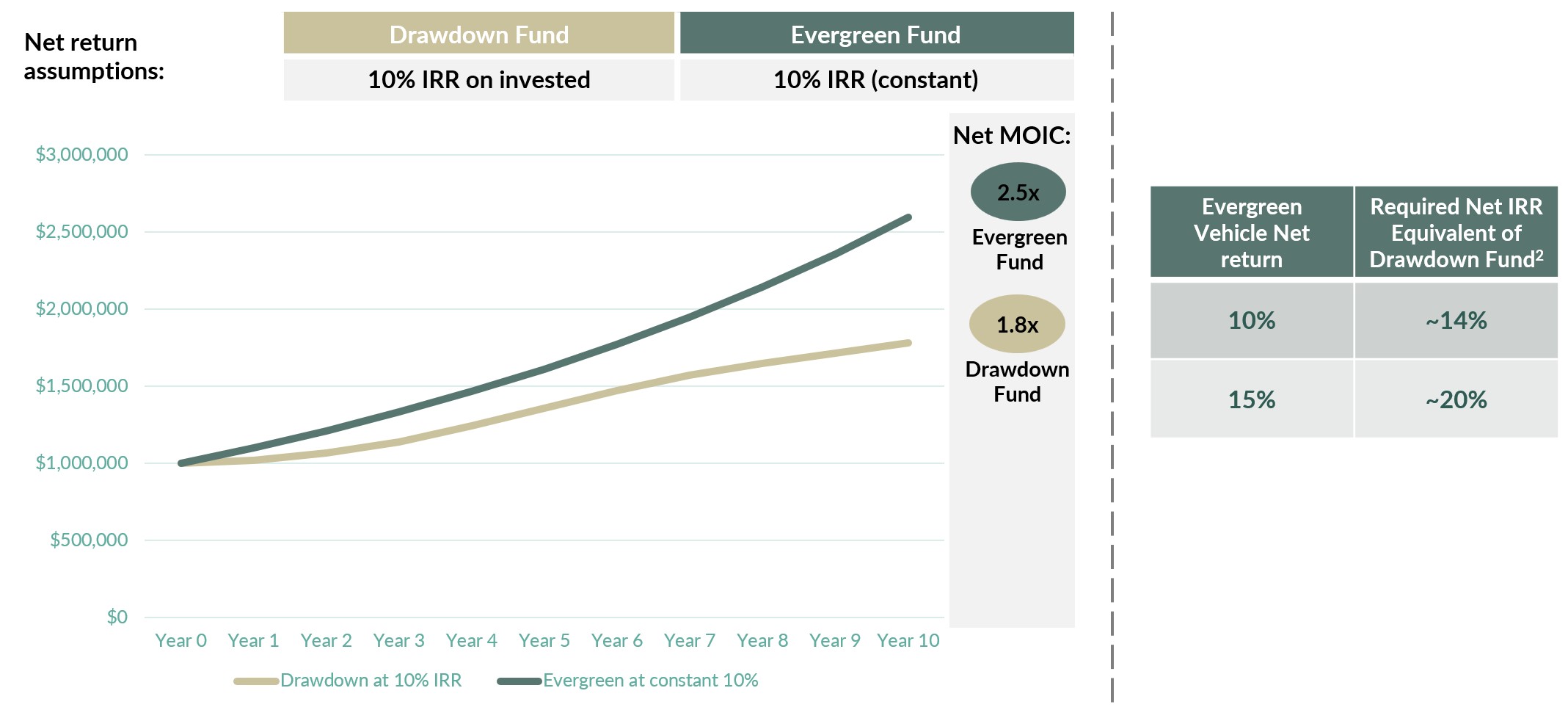

We have often articulated our preference for strategies, such as private credit, where one can benefit from immediate compounding of assets, rather than drawing down capital over a period of 3-4 years. In this way, funds with a lower headline IRR can in fact deliver a higher multiple on invested cash at the end of the life of a typical drawdown structure, as illustrated below.

Source: Capricorn Private Investments, Apollo Global Management

Understanding client objectives remains fundamental

While it is common for private investment offices to remark that there is ‘no one size fits all’ approach for individual families, it bears repeating. High allocations to private equity and other illiquid assets are simply not appropriate for all clients, despite our continued belief that select managers and strategies can still deliver long-term capital growth above that of public markets.

Ultimately, most families are not endowments, and very few have the luxury of ‘perpetuity capital’, as Oxford University refers to its own endowment. Most families want to minimise complexity where possible, meaning the extreme level of illiquidity seen in larger endowment portfolios is neither desirable nor appropriate for typical family office portfolios.

At the outset of our client relationships we rigorously and repeatedly assess the purpose of a client’s asset pool, along with the ability to tolerate risk and illiquidity, before constructing an investment policy statement. We advocate avoiding unnecessary layers within portfolios – keeping allocations to a smaller number of high conviction positions in active managers, complemented with lower-cost allocations in liquid asset classes where outperformance is generally harder to come by.

Ultimately, we see the term ‘Endowment Model’ as a useful shorthand for an approach we believe remains sound: seeking long-term compounding of returns by staying invested, seeking to limit drawdowns through portfolio diversifiers, and – particularly relevant today – rebalancing judiciously during periods of market extremes. We see these fundamental points as no less relevant today than forty years ago when the ‘Yale model’ was born.